Guangdong Wenshi Food Group Co., Ltd. Long-term Credit Rating Report

2021-10-04 22:20:08

The rating opinion of Joint Credit Rating Co., Ltd. (hereinafter referred to as “Joint Creditâ€) on the Guangdong Wenshi Food Group Co., Ltd. (hereinafter referred to as the “Companyâ€) reflects the company as a leading enterprise in the aquaculture industry, in the scale of aquaculture, breeding technology, business model , profitability and solvency. The joint credit letter also noted that there are market risks and outbreak risks in the breeding industry companies, but the company has a certain scale of economic advantages, a high level of aquaculture technology, coupled with its "integrated" business model of aquaculture and feed processing to help protect against market risks, and The formation of support for the company's overall credit level.

The rating opinion of Joint Credit Rating Co., Ltd. (hereinafter referred to as “Joint Creditâ€) on the Guangdong Wenshi Food Group Co., Ltd. (hereinafter referred to as the “Companyâ€) reflects the company as a leading enterprise in the aquaculture industry, in the scale of aquaculture, breeding technology, business model , profitability and solvency. The joint credit letter also noted that there are market risks and outbreak risks in the breeding industry companies, but the company has a certain scale of economic advantages, a high level of aquaculture technology, coupled with its "integrated" business model of aquaculture and feed processing to help protect against market risks, and The formation of support for the company's overall credit level. In the live pig breeding cycle, population-cost-profit changes have a gradual impact on the price structure. In addition, the government's efforts to regulate and control increase the price of pork. In the future, the company will continue to expand its aquaculture scale and appropriately develop high value-added extension industries related to aquaculture. The company's operating performance is expected to maintain growth. Joint Credit Ratings has a stable outlook for the company.

Advantage 1, the company as a leading enterprise in the breeding industry, a higher level of aquaculture technology, and the implementation of the "integration" of aquaculture and feed processing operations, the overall strong anti-risk capabilities.

2. The "corporate + farmer" operating and breeding mode is conducive to the company's large-scale breeding. At the same time, the company sets up a better return mechanism for farmers, which is conducive to the stability of their business model.

3, the company's equity incentive mechanism is conducive to improving employee enthusiasm and team stability.

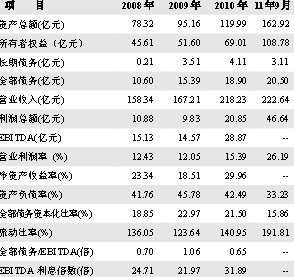

4. Affected by the market supply and demand, the price of broiler hogs increased, the company’s operating income and profits increased substantially, and profitability improved significantly.

5. The owners’ equity of the company has increased significantly and the debt burden is lighter.

Concern 1, the company's breeding industry market and the risk of epidemic situation is relatively large;

2. The price of soybean meal and corn has fluctuated greatly in the past two years, making it more difficult to control the cost of animal husbandry and breeding enterprises;

3. As the company's branches and management levels continue to increase;

The increase in administrative expenses is relatively large, and the overall management and management efficiency of the company needs to be further improved.

| Product Description | |

| Name | Canned Pink Salmon |

| Flavor | Brine, Oil |

| Type | Bone-in and skin-on, bone-less and skin-less |

| Certificates | EU, FDA, BRC, HALAL,HACCP,KOSHER |

| Net weight | 170g, 185g, 400g, 417g, 425g, 1kg, 1.88kg. |

| Brand | Our brand or OEM, ODM |

| Shelf life | 3/4 Years |

| MOQ | 1X20'FCL |

| Payment terms | T/T, L/C |

| Delivery time | 25 days after label artwork confirmed and advance payment done. |

| Packing | normal lid or easy open,paper label or lithio can, paper carton or shrinked by tray |

| EU NO. | 3302/01034 |

| RUSSIA NO. | 3302/01034 |

| Shipping docs | Commercial Invoice |

| Packing List | |

| Bill of Lading | |

| Certificate Of Origin/ Form A | |

| Health Certificate | |

| Veterinary Certificate | |

| Catching certificate | |

| Or as per customer`s request | |

Canned Smoked Salmon,Canned Pink Salmon,Pink Salmon In Brine,Pink Salmon In Vegetable Oil

Tropical Food Manufacturing (Ningbo) Co., Ltd. , https://www.tropical-food.com